Canada and Venezuela fill Critical role in Strait of Hormuz blockage

The US is Self-Sufficient in Gasoline but not Diesel - The "Workhorse of the Economy"

Summary:

You’ve probably heard that the US is “energy independent.” **

In actuality the US is “net energy independent,” if taking into account US imports from the Middle East, Canada, and Venezuela and exports to Europe and Asia. These imports and exports are necessary to accommodate the mismatch between the types of oil we use and produce, and type of oil our refineries are configured to refine.

We are self-sufficient in gasoline but not diesel or jet fuel.

“Because diesel is the literal “workhorse” of the modern economy, a shortage doesn’t just make commuting more expensive—it creates a cascading failure across nearly every physical supply chain.”

Logistics - like a “Cardiac Arrest” (trucks)

Agriculture (fertilizer, tractors, harvesters)

Construction & Infrastructure Stagnation

Emergencies & Power Backup

19% of US usage is diesel, or 3.9 - 4 million barrels per day.

9% of US usage is jet fuel, or 1.7 - 1.8 million barrels per day

(See detail below)

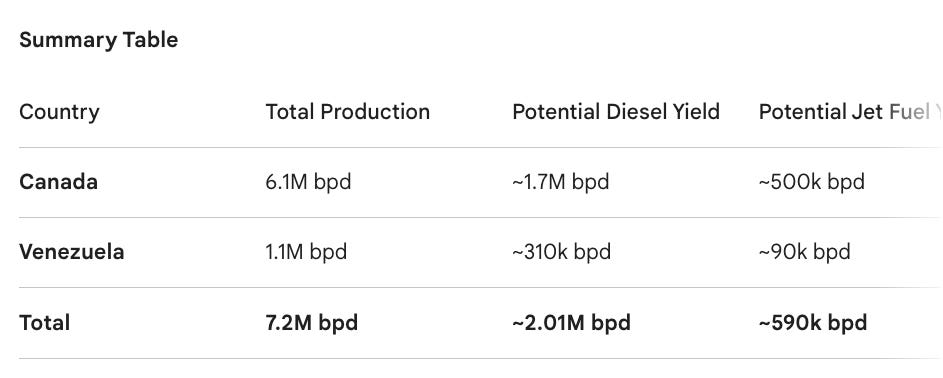

Canadian and Venezuelan oil is, the right type of oil to produce diesel.

“As of late March 2026, Canada and Venezuela are the primary “heavy lifters” of the Western Hemisphere’s energy supply. While their total oil production is massive, the amount of diesel and jet fuel they provide depends heavily on the complexity of the refineries that process their crude.”

This will likely lead to increases in the price of airfare, and everything transported by diesel truck or tractor (food, etc). Gasoline should be less affected.

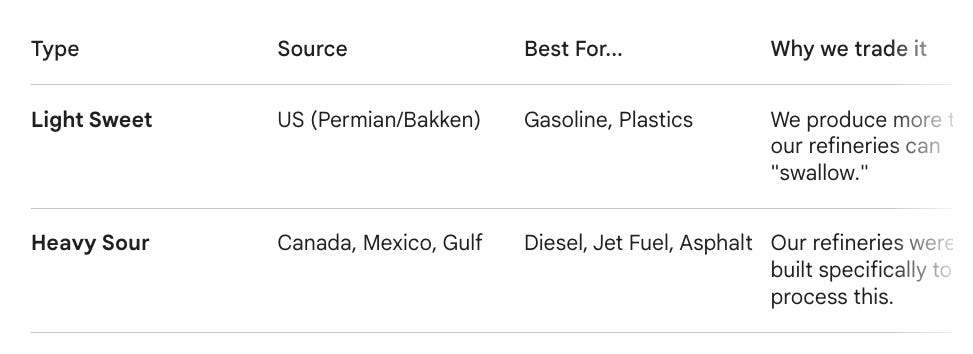

“The reason these two countries are so critical during the Strait of Hormuz blockage is that their oil is chemically “heavy.””

“Diesel Density: Unlike light U.S. shale oil, which is great for gasoline, Canadian and Venezuelan crudes have the long-chain hydrocarbons required to produce high volumes of diesel and jet fuel.”

“The Swap: Without this heavy oil, U.S. refineries struggle to produce enough diesel for the trucking industry, even if they have a surplus of light oil for cars.”

Detail: AI Conversation:

https://gemini.google.com/share/e290d9c0e3ce. (full)

Highlights:

Q: What shortages of goods and services are expected in the US due to the Strait of Hormuz blockage?

A: Energy and Fuel Shortages

Although the U.S. produces much of its own oil, it relies on specific heavy crude grades from the Middle East to feed many of its refineries, which are configured for that type of oil.

Refined Products: Shortages of heavy crude are leading to lower yields of diesel and jet fuel.

..

Q: What would be the consequences of diesel fuel shortages?

A: Because diesel is the literal “workhorse” of the modern economy, a shortage doesn’t just make commuting more expensive—it creates a cascading failure across nearly every physical supply chain.

As of late March 2026, with the Strait of Hormuz remaining a major bottleneck, the consequences are manifesting in four critical stages:

1. The Logistics “Cardiac Arrest”

Over 90% of U.S. freight moves by truck, and almost all of those trucks run on diesel.

Reduced Delivery Frequency: Retailers are shifting from “just-in-time” to “when-possible” delivery. You’ll notice more out-of-stock signs for non-essential items as carriers prioritize high-margin or essential goods.

Fuel Rationing: In some regions, truck stops have reportedly limited fills to 40–50 gallons (far below the 200+ gallon capacity of a long-haul rig), forcing drivers to stop more frequently and extending 2-day trips into 4-day treks.

The “Surcharge” Spiral: Shipping companies are passing 20–30% fuel surcharges to wholesalers, who pass them to retailers, who pass them to you.

2. Agricultural Disruption (The “Silent” Crisis)

Diesel is the primary fuel for tractors, harvesters, and the trucks that move grain to silos.

Planting Delays: We are currently in the spring planting window. Shortages of “off-road” diesel (the dyed, untaxed fuel used by farmers) can lead to missed planting windows, which permanently reduces the year’s total crop yield.

Livestock Costs: The cost of transporting animal feed has skyrocketed. This usually leads to a “culling” phase where farmers sell off livestock early because they can’t afford to feed them, leading to a temporary dip in meat prices followed by a massive, long-term spike.

3. Construction and Infrastructure Stagnation

Unlike passenger cars, heavy machinery (excavators, cranes, bulldozers) cannot easily be electrified.

Project Halts: Major infrastructure projects—roads, bridges, and housing—are seeing “delay surcharges” or total work stoppages as contractors wait for fuel deliveries.

Escalation Clauses: Many construction contracts are being triggered, allowing builders to raise prices mid-project to cover the 40%+ increase in diesel costs seen since early 2026.

4. Emergency Services and Power Backup

This is the most critical “safety” consequence.

Backup Generators: Hospitals, data centers, and water treatment plants rely on massive diesel generators for backup power. A prolonged shortage risks the reliability of these “last line of defense” systems.

Emergency Response: While many police cruisers run on gasoline, fire trucks and ambulances are almost exclusively diesel-powered. Some municipalities are already moving to “priority refueling” status to ensure emergency fleets remain operational.

Oil Quality Varies by density and sulfur content

It might seem counterintuitive for the world’s largest oil producer to also be a major importer, but the U.S. oil industry operates like a specialized kitchen. Just because you grow a lot of wheat (light oil) doesn’t mean you can stop buying milk and eggs (heavy oil) if you want to bake a variety of cakes.

As of early 2026, this “mismatch” is the primary reason why a blockage in the Strait of Hormuz still hurts the U.S. economy despite our record domestic production.

1. The Refinery Mismatch (Quality Matters)

Oil isn’t a single uniform liquid; it varies by density (API gravity) and sulfur content (”sweet” vs. “sour”).

What the U.S. Produces: The vast majority of U.S. shale oil is Light, Sweet Crude. It’s easy to refine into gasoline and jet fuel but lacks the “heavier” molecules needed for high-quality diesel and asphalt.

What U.S. Refineries Need: Decades ago, U.S. refineries (especially on the Gulf Coast) invested billions to process Heavy, Sour Crude from places like Saudi Arabia, Iraq, Mexico, and Canada. These complex machines—called “crackers” and “cokers”—actually run less efficiently if you feed them only light U.S. oil.

2. The Product Yield (Diesel vs. Gasoline)

Refining is about “yield”—the percentage of different fuels you get from one barrel.

Heavy oil (imported) is better for making diesel, heating oil, and marine fuel.

Light oil (domestic) is excellent for making gasoline and naphtha (used in plastics).

By importing heavy crude and exporting our surplus light crude, U.S. refiners can “balance the slate” to maximize the production of the specific fuels the market demands at that moment.

3. Geography and Logistics

It is often cheaper to move oil across an ocean than across the United States.

The Pipeline Problem: Because of the way U.S. pipeline infrastructure is built, it’s sometimes more economical for a refinery in the Northeast (PADD 1) to import oil from overseas than to pay for rail or tanker transport of North Dakota shale oil across the country.

The Jones Act: A century-old law requires goods shipped between U.S. ports to be carried on U.S.-built and crewed ships. Since there are very few U.S.-made oil tankers, it is often significantly cheaper to hire a foreign tanker to bring oil from the Middle East to California than to bring it from Texas to California.

4. Why We Export

Since U.S. refineries can only “eat” so much light oil before they hit their technical limits, the U.S. exports the extra.

Global Demand: Refineries in Europe and Asia that aren’t as complex as ours prefer light oil because they don’t have the expensive equipment to handle the “dirty” heavy stuff.

The 2026 Shift: With the 2026 construction of new “shale-specific” refineries (like the recently announced project in Brownsville, Texas), the U.S. is slowly trying to close this gap, but re-tooling the entire national refining system takes decades.

Summary of the “Oil Swap”

Q: How much oil does Venezuela produce and how much could it produce in 6 months if there were a large investment in increasing capacity?

As of late March 2026, Venezuela’s oil production is experiencing a fragile but notable uptick due to shifting geopolitical dynamics and the global energy crisis caused by the Strait of Hormuz blockage.

Current Production (March 2026)

According to recent reports from PDVSA and OPEC, Venezuela is currently producing approximately 1.1 million barrels per day (bpd).

This is a significant increase from the 800,000–900,000 bpd range seen at the start of the year.

The recovery has been driven by a temporary easing of logistical constraints, improved access to “diluents” (thinning agents needed to move heavy sludge-like crude through pipelines), and a rush by Western firms to secure alternative heavy crude sources.

Q: How much diesel and jet fuel does the US use, as compared with gasoline and other oil uses?

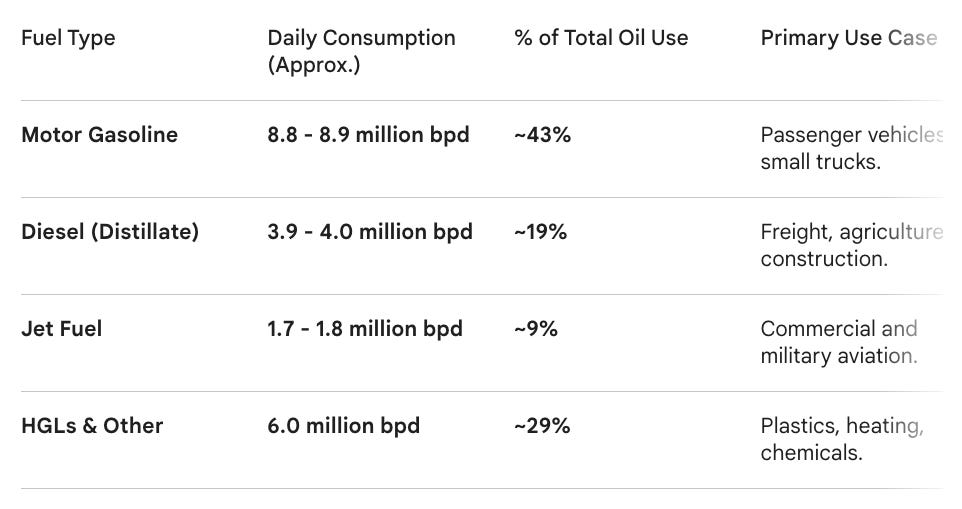

To understand the impact of the current energy crisis, it’s helpful to look at the U.S. as a massive engine with a very specific fuel diet. While the U.S. consumes about 20.6 million barrels of oil per day (bpd) in 2026, that “barrel” is split into several distinct products.

The following data reflects current 2026 consumption estimates and the relative “weight” each fuel has in the U.S. economy.

1. The Consumption Breakdown (2026 Estimates)

Gasoline remains the undisputed king of U.S. oil use, but diesel and jet fuel are the sectors most vulnerable to the current Strait of Hormuz disruption due to their reliance on heavier imported crudes.

2. Gasoline: The Declining Giant

While gasoline accounts for nearly half of every barrel, its dominance is slowly eroding.

Efficiency Gains: Better engine standards and the continued rise of EVs have caused gasoline demand to “plateau.”

Current Status: In March 2026, demand is steady but sensitive to the $3.30+ per gallon average retail prices caused by the global risk premium.

3. Diesel: The Economic Workhorse

Diesel is the fuel most affected by the Hormuz blockage because U.S. refineries often need heavy, sour crude (the kind typically blocked in the Gulf) to produce high yields of high-quality diesel.

Economic Link: Diesel demand is almost perfectly correlated with GDP. If trucks aren’t moving, the economy isn’t growing.

Current Crisis: Because diesel inventories were already at multi-year lows entering 2026, the shortage of heavy crude imports has pushed retail diesel prices toward $4.12 per gallon, significantly higher than gasoline.

4. Jet Fuel: The “Full Recovery” Sector

Jet fuel has seen the most aggressive growth in the last two years as international travel finally surpassed 2019 levels.

Sensitivity: Aviation is highly sensitive to “crack spreads” (the difference between the price of crude oil and the refined product).

Supply Tightness: Refineries can often choose to produce either more diesel or more jet fuel from the same part of the barrel. With the current diesel shortage, jet fuel production is being “squeezed,” leading to higher ticket prices and potential flight consolidations this summer.

5. Other Oil Uses (The “Hidden” 30%)

A huge portion of U.S. oil consumption isn’t “burned” in an engine at all.

Hydrocarbon Gas Liquids (HGLs): This includes propane and ethane. Much of this goes into the petrochemical boom to create plastics, resins, and synthetic fibers.

Residual Fuel Oil: Used for massive container ships and some power generation.

Key Comparison: Why Diesel and Jet Fuel Matter More Right Now

While gasoline makes up more of the volume, the U.S. is essentially self-sufficient in the “light” crude needed for gasoline. We are not self-sufficient in the “heavy” crude needed for diesel and jet fuel. This is why the Hormuz blockage feels like a “diesel crisis” more than a “gasoline crisis” at the local level.