How Plans to Privatize Forests and Lakes would be implemented using Blockchain

Carbon Credit markets would "solve" global warming by selling the right to CO2 pollution.

Did you know that there is a top-down “movement” to “tokenize” or sell fractional shares to natural resources like forests and lakes, as well as physical assets like buildings and fine art paintings? This top-down movement is led by institutions like:

The World Economic Forum, World Bank,

Goldman Sachs, JPMorgan, HSBC, BlackRock, Franklin Templeton, McKinsey.

US Federal Reserve, US SEC , The Bank of England, and European Investment Bank

This “movement” seems to operate under the theory that private owners will take better care of the property and natural word if it is all privately owned, and that fractional shares, called tokens, will make ownership participation accessible to the average person.

Carbon Credits

The creation of a carbon markets based on the sale of credits to emit carbon is one instance of financialization. It’s intent is to solve climate change by improving markets.

The website carboncredits.com says that the average American “generates 16 tons of CO2 a year through driving, shopping”, etc.

Another metric for understanding what 1 ton of CO2 is — you would generate one ton of CO2 by driving your average 22 mpg car from New York to Las Vegas

The government in this model is like a clockmaker who sets up a system and then lets that system play out with minimal interference. It would limit the overall amount of CO2 consumption by issuing an allowance of credits individuals/companies and then allow these people and individuals to buy and sell the number of credits required by their actions.

The theory behind carbon credits is that people and companies would have an incentive to reduce their carbon use because they can sell excess credits to those who want to pollute more than their allowance.

Tokenization

More private ownership of resources like forests and lakes is theorized as better because the owners would be better incentivized to protect nature. Under the “tokeniztion” system, investors could buy a token (or fraction) of a share of a lake or a building for small amounts of say, $100, rather than having to purchase the entire lake, painting, or building which may cost hundreds of thousands or millions of dollars. A lake may thus have many shareholders. A homeowner could also easily sell a fraction of their home equity if desired.

The ownership data for all these fractional shares is intended to be stored on blockchains like Bitcoin or a crypto like Etherium that store their records in distributed ledgers.

My Thoughts:

A friend described this carbon credits system as the equivalent of digital indulgences — like those permits granted by the Catholic Church for the remission of sins. It was indulgences that so outraged Martin Luther and inspired the reformation.

The fractional ownership of property is an attempt to “improve” our current property system by taking neoliberal capitalism to its logical extreme.

Questions

How much do people you know know about tokenization — fractional ownership in property like buildings, water, land, etc?

How much money is to be made by financial companies to administer this? Will it work? Is it worth it?

The system is being enacted from the top down. Is more public participation needed to grant these ideas legitimacy?

What, if anything, should be done to ensure this system reflects the public interest, broadly defined?

What do you think about following ideas to the logical extreme? Does extremism work in the case of capitalism?

A Critical Video:

DETAIL: AI Summary:

Q: What is asset tokenization?

Content Authors:

McKinsey

Dante Disparte & Gordon Liao, World Economic Forum

World Economic Forum

BCG, Aptos Labs, and Invesco

At its core, asset tokenization is the process of converting the ownership rights of a physical or digital asset into a digital token on a blockchain.

Think of it like a digital “certificate of authenticity” and “deed of ownership” rolled into one. Instead of having a paper contract that says you own 10% of a building, you have a digital token in your wallet that represents that same 10%.

How It Works

The process typically follows three main steps to move an asset from the “real world” onto the digital ledger:

Asset Identification: Determining the value and legal status of the asset (e.g., a piece of fine art, a gold bar, or a startup’s equity).

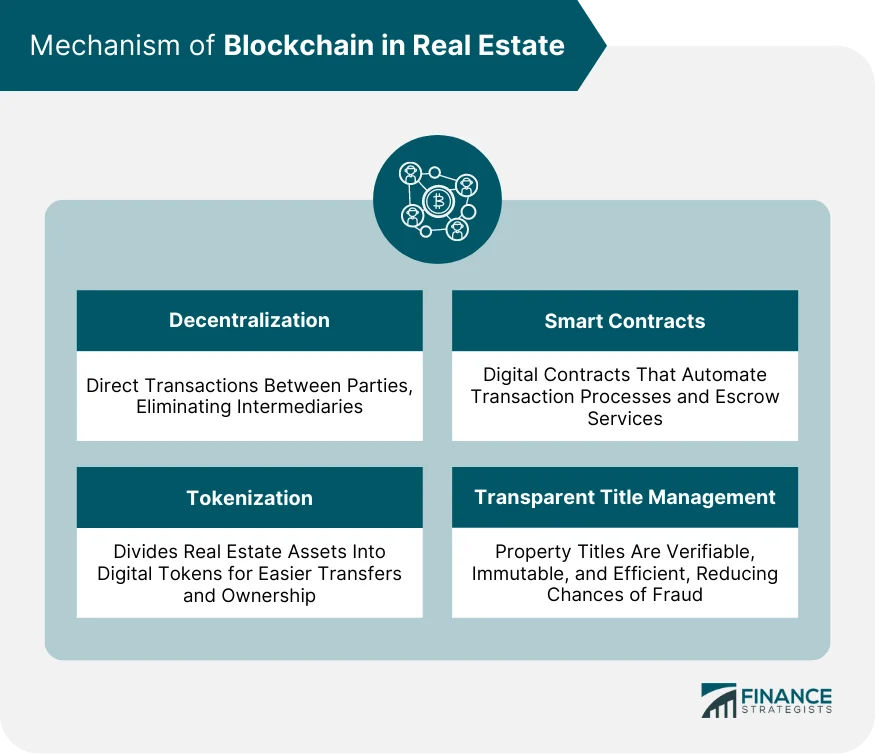

Smart Contract Creation: Coding the rules of the asset into a smart contract. This includes how many tokens exist, what rights the holder has (like dividends), and how the tokens can be traded.

Token Issuance: The tokens are minted on a blockchain (like Ethereum or Polygon) and distributed to investors.

Why Tokenize?

Tokenization is gaining massive traction because it solves several “old world” financial problems:

Fractional Ownership: You might not have $50 million to buy a skyscraper, but you might have $500 to buy a “sliver” of it. Tokenization lowers the barrier to entry for expensive assets.

Increased Liquidity: Real estate or fine art are “illiquid,” meaning they take months to sell. Tokens can be traded 24/7 on secondary markets, making it much faster to cash out.

Transparency: Because the blockchain is a public ledger, ownership history and transaction records are immutable and visible to everyone, reducing fraud.

Efficiency: By using Smart Contracts, you remove the need for many “middlemen” (like escrow agents or manual clearinghouses), which lowers transaction fees.

MORE:

The push to adopt “tokenization” as the next phase in financial system is being led by those at the “top.”

This could result in a legal framework for “assets” like art and real estate being chopped up into individual shares and natural assets like lakes or forests being “tokenized” as a new form of environmental policy. This policy is done under the theory that all natural assets would be taken better care of, if the were subject to clear ownership rights.

Who is behind this:

It could also result in expanded profits to “WallStreet” institutions.

Global Institutions: Bank of England, Euroclear, DTCC, World Bank, and the European Investment Bank

Financial Institutions: BlackRock, J.P. Morgan, Franklin Templeton, HSBC, and Goldman Sachs are deploying tokenized funds, bonds, and securities, demonstrating a coordinated push to integrate blockchain into traditional finance

Some commentators say that Etherium and Bitcoin could be used to store token ownership. (How to Tokenize Real-World Assets on Bitcoin)

1) "From Ripples to Waves: The Transformational Power of Tokenizing Assets"

By McKinsey & Company (June 2024)

🔹 What Is Tokenization?

Tokenization is turning real-world assets (like stocks, bonds, or real estate) into digital tokens on a blockchain.

These tokens represent ownership and can be traded instantly, fractionalized, and tracked securely.

Think of it as turning a physical thing (like a $10 million property) into digital Lego pieces that can be traded by anyone, anytime.

🔹 Why Does Tokenization Matter?

Tokenization could:

Make finance faster and cheaper (instant settlement, lower fees)

Improve transparency (every transaction is trackable on blockchain)

Allow smaller investors access to big-ticket assets (like rare art or private equity)

Simplify compliance and reporting with programmable rules built into tokens

McKinsey compares this potential to other major financial shifts like:

Online banking

Mobile payments

The rise of ETFs

🔹 Who Benefits?

Asset Managers: Can cut costs, reach new investors, and offer innovative products

Investors: Gain more control, faster access, and broader choices (e.g., fractional ownership in rare assets)

Banks and Custodians: Could evolve from middlemen to tech-enabled service providers

🔹 What's the Current Reality?

Still early. Tokenized finance is mostly in pilot programs or small-scale trials.

Less than 1% of total assets are tokenized today.

But interest is growing, especially in:

Private funds

Alternative assets

Government-backed digital currencies (CBDCs)

🔹 What’s Holding It Back?

Fragmented regulations (rules vary by country)

Lack of shared standards across platforms

Legacy systems in finance that don’t talk well with blockchain tech

Skepticism from traditional players

🔹 What Needs to Happen?

McKinsey says the industry needs:

Clear regulation to protect investors without stifling innovation

Unified standards so different token systems can work together

Collaboration between tech firms, regulators, and financial institutions

More proof that tokenized systems are secure and scalable

🔹 What’s the Outlook?

McKinsey believes tokenization could move from a niche experiment to a major force within 5–10 years, if:

Financial institutions act decisively

Regulators build supportive frameworks

Technology proves reliable at scale

💡 Key Takeaway:

“Tokenization has the potential to reshape asset management—cutting costs, expanding access, and unlocking new ways to invest. But it won’t happen automatically. Industry players must move quickly to make it real.”

2) “Code as Law”: The Tokenization of Financial Assets and the Paradox of Programmability

By Dante Disparte & Gordon Liao – October 28, 2024 (World Economic Forum)

🌐 What Is This About?

This article explains how tokenization — turning real-world financial assets into blockchain-based tokens — is changing the financial system. But there's a twist: the very feature that makes tokenization powerful — programmability — also creates risks and regulatory challenges.

💡 Key Concepts Explained

1. Tokenization

This means putting traditional assets (like bonds or deposits) on a blockchain, allowing for fast, secure, and digital trading.

2. Programmability

This means embedding rules directly into the token, so it can behave automatically (like: “If X happens, then do Y”).

This is similar to smart contracts in crypto.

⚖️ The Paradox of Programmability

Why It’s Powerful:

Increases automation, efficiency, and transparency.

Enables faster payments, settlements, and risk controls (e.g., automatic payment only when both sides deliver).

Why It’s Risky:

Removes human discretion — intermediaries can’t easily override automated rules.

Can cause market instability, like automated bank runs or herd behavior when small risk signals get amplified by code.

🏦 How It Affects Banks and Regulators

Banks that tokenize deposits must deal with faster-moving money and higher volatility.

Regulators are unsure how to classify these assets — they blend finance and technology in new ways.

The "singleness of money" (one dollar = one dollar everywhere) could be challenged if stablecoins or tokenized deposits deviate in value.

🧠 Real-World Implications

Narrow Banking:

To avoid risks, banks may adopt simpler, safer balance sheets with only short-term, high-quality assets.

This mimics money market funds and stablecoin models, where risk is minimized but flexibility is reduced.

Separation of Payment vs. Savings:

To prevent “code-triggered” bank runs, tokens used for payments may need to be separated from interest-earning tokens (e.g., stablecoins vs. tokenized savings).

🧾 “Code as Law” — What It Means

When rules are written directly into the code, it becomes the law of the transaction.

This reduces risk of human fraud or misjudgment.

But it also makes it harder for institutions to differentiate themselves, leading to more commoditization of financial services.

🔄 Long-Term Impact

Tokenization could reshape finance by:

Making illiquid assets more liquid.

Moving away from traditional banks to automated, market-based systems.

Reducing the discretion of financial intermediaries.

But to realize these benefits, regulators must focus on regulating the activity, not just the technology.

📌 Bottom Line

Tokenization + Programmability = Huge potential + New risks.

Automation boosts speed and transparency but may reduce flexibility and increase volatility.

Regulators and institutions must tread carefully.

Would you like a visual infographic of this summary or a comparison with the McKinsey or BCG tokenization reports?

3) How tokenization is transforming global finance and investment

World Economic Forum

Definition & Shift:

Tokenization refers to creating digital representations of physical or financial assets on the blockchain. After years of testing and development, governments and major financial institutions are now actively implementing tokenization, marking a turning point in global finance.

Problem It Solves:

Current financial systems are fragmented and outdated, making asset ownership and trade inefficient. Tokenization promises real-time settlement, transparency, and interoperability across markets.

Major Developments:

Institutions leading the charge: Bank of England, Euroclear, DTCC, World Bank, and the European Investment Bank are rolling out tokenized financial systems.

Corporate initiatives: Goldman Sachs and HSBC have deployed tokenized bond platforms; BlackRock and Franklin Templeton have launched tokenized mutual funds.

Global innovations: The Hong Kong Monetary Authority issued multicurrency tokenized green bonds using blockchain platforms in 2023–2024.

Benefits of Tokenization:

Estimated $15–20 billion in global annual savings from operational efficiency

Up to $100 billion in capital freed through better collateral management

Faster, 24/7 settlement cycles reduce risk and increase market liquidity

Unlocks trillions in idle collateral (only ~$29T of $255T is used today)

Challenges & Governance:

Key concerns include security, privacy, and ledger governance. The article emphasizes the need for neutral, international oversight bodies—such as the Linux Foundation-backed Global Synchronizer Foundation—to ensure transparency and compliance in managing decentralized financial infrastructures.

Conclusion:

Tokenization has moved from theory to reality. As adoption scales, it will fundamentally reshape global capital markets—making them more efficient, connected, and inclusive.

4) Tokenized Funds: The Third Revolution in Asset Management Decoded

By BCG, Aptos Labs, and Invesco — October 2024

Executive Summary

Tokenized funds represent a transformative use of blockchain in financial services. By digitizing fund ownership on public-permissioned blockchains, tokenization enables 24/7 trading, fractional ownership, instant settlement, and programmable compliance—unlocking value for investors and financial institutions. This could result in an estimated $100 billion in extra annual returns for investors and $400 billion in new financial opportunities.

Key Concepts and Takeaways

1. What is Fund Tokenization?

Blockchain-based digital tokens represent fund shares.

Comparable to current fund structures (e.g., mutual funds), but with real-time capabilities.

Does not require major legal structural changes (unlike tokenized real estate).

2. Benefits for Investors

Instant settlement: Unlocks trapped capital, reducing friction from T+2/3 delays.

Lower fees: Potential to save $33B annually due to ETF-like secondary trading.

Liquidity: Tokenized shares can be used as collateral in lending.

Intra-day NAV trading: Allows advanced investors to arbitrage price swings for gains ($80–400B potential).

Access: Lower investment minimums and micro-investing for retail users.

3. Opportunities for Financial Institutions

Tap into $290B of existing crypto-native demand for yield-bearing assets.

Future-proof against on-chain TradFi money (CBDCs, tokenized deposits).

New revenue models: Embedded investing, personalized portfolios via smart contracts, 24/7 services.

Enhance distribution and user experience for younger and digitally-native investors.

Market Potential and Growth Path

Current Tokenized Fund AUM (2024): ~$2B

(e.g., BlackRock’s BUIDL and Franklin Templeton’s FOBXX)Projected AUM by 2030:

Base case: $600B–$1T

If existing funds convert: $Trillions+

Catalysts: Regulated stablecoins, tokenized deposits, CBDCs, interoperable tech

Implementation Models

There are three main approaches:

Digital twins: Tokenize existing funds via parallel operations.

Native tokenized vehicles: Designed from scratch for blockchain.

Conversions: Transform traditional funds into tokenized form.

Technology and Compliance Blueprint

Modular Stack:

Asset Layer (funds, stablecoins, deposits)

Business Solutions (lending, collateralization, micro-investing)

Permission Control (KYC, smart contract rules, compliance)

Blockchain Infrastructure (public-permissioned preferred)

Security & Privacy Requirements

Encryption, access controls, disaster recovery, and regulatory compliance (KYC/AML).

Public-permissioned blockchains like Aptos offer the benefits of decentralization with institutional-grade controls.

Cost Considerations

Transaction ("gas") fees must stay under ~$0.10 to be commercially viable.

Some public chains already offer gas fees below $0.001.

Strategic Playbook for Institutions

To succeed, firms must address:

Vision: Identify competitive advantage and transformation roadmap.

Compliance: Ensure regulatory adherence and data privacy.

Interoperability: Use cross-chain and global standards.

Use Case Sequencing: Prioritize highest ROI opportunities.

Tech & Ops: Upgrade infrastructure with modular, scalable systems.

Center of Excellence (CoE): Drive internal alignment and adoption.

Conclusion

The whitepaper frames tokenized funds as the next major leap in asset management after mutual funds and ETFs. With the right technology, regulatory clarity, and coordination, the industry can unlock hundreds of billions in value while delivering a more efficient, inclusive, and programmable financial system.

5) Google AI: Who is pushing for the tokenization of financial assets?

Major financial institutions, governments, and technology providers are actively pushing for the tokenization of financial assets. Wall Street giants like BlackRock, J.P. Morgan, and Franklin Templeton are leading the charge, with BlackRock launching its first tokenized fund on a public blockchain and J.P. Morgan developing services to tokenize assets like carbon credits.238 This institutional momentum is supported by global financial bodies such as the World Bank, the European Investment Bank, and the Bank of England, which are building technology and launching tokenized assets.2 The trend is further amplified by platforms like Robinhood and Coinbase, which are rolling out or seeking approval for tokenized stocks, while regulators and central banks worldwide are engaging with the technology to modernize financial infrastructure.2311

Major Financial Institutions: BlackRock, J.P. Morgan, Franklin Templeton, HSBC, and Goldman Sachs are deploying tokenized funds, bonds, and securities, demonstrating a coordinated push to integrate blockchain into traditional finance.239

Government and Central Bank Initiatives: The Bank of England, World Bank, European Investment Bank, and the U.S. Federal Reserve are actively involved in developing central bank digital currencies (CBDCs) and tokenized asset platforms, signaling strong governmental support.25

Technology and Infrastructure Providers: Companies like Securitize, Ondo Finance, and TZERO are building the underlying platforms and networks, such as the TZERO Chain, to power regulated asset tokenization at scale.23

Regulatory and Industry Collaboration: The U.S. Securities and Exchange Commission (SEC) is engaging with Ethereum, and the White House has recognized the strategic importance of real-world asset (RWA) tokenization, indicating a growing regulatory acceptance.23