The Hormuz Toll and the End of the Petrodollar

How Iran’s Yuan Mandate is Influencing the Fed Decision to Reconsider the 2% Inflation mandate

AI Summary:

For decades, the “Petrodollar” was a pillar of American power—an unwritten rule that global oil must be traded in U.S. dollars, ensuring a constant flow of capital into U.S. Treasury bonds. In early 2026, that pillar has been violently shaken. Following the outbreak of the U.S.-Israeli conflict with Iran in February, Tehran has transformed the Strait of Hormuz from a shipping lane into a geopolitical financial checkpoint.

The “Yuan-for-Passage” Mandate:

In March 2026, Iran began implementing a selective blockade of the Strait. While U.S. and Israeli-linked vessels are barred entirely, Tehran has signaled a “Green Lane” for tankers that settle their oil transactions in Chinese Yuan. This “Hormuz Toll” has forced several major Asian importers to bypass the dollar system to ensure their energy security. By early April, reports indicated that at least 13 million barrels of oil had already transited the Strait under these new, non-dollar terms.

{kind=link}

The Economic Chain Reaction:

The Death of “Automated” Demand: As Persian Gulf producers accept Yuan to maintain access to Chinese markets and avoid Iranian interference, they are no longer “recycling” their profits into U.S. Treasuries. This has created a massive hole in the U.S. government’s borrowing plan.

Interest Rate Pressure: To attract new buyers for its $39 trillion debt, the U.S. Treasury has been forced to keep interest rates at multi-year highs. This “higher-for-longer” environment is the direct result of the dollar losing its monopoly on the oil trade.

The Fiscal Squeeze: With the U.S. now spending over $1.1 trillion annually on interest payments alone, the government is caught in a “debt trap.” Every dollar spent on interest is a dollar not spent on infrastructure or defense, while the “Short-term T-bill” strategy used to keep the lights on has made the entire U.S. budget hyper-sensitive to any further rate spikes.

The Bottom Line: Iran’s move to mandate the Yuan in the Strait of Hormuz is more than a wartime tactic; it is an asymmetric strike on the dollar’s “exorbitant privilege.” For the average American, this shift is no longer a distant policy debate—it is the invisible force keeping mortgage rates high and the cost of living elevated as the world transitions to a “multipolar” financial era.

Q: If Persian Gulf oil producers begin selling their oil in Chinese Yuan instead of US Dollars what will be the effect on the dollar, US interest rates, and the ability of the US government to borrow money through treasuries?

AI Response:

The shift toward “Petroyuan” (oil traded in Chinese Yuan) represents a challenge to the Petrodollar system—a decades-old arrangement where global oil is priced in USD, forcing nations to hold dollars and reinvest them in US debt.

If Persian Gulf producers (like Saudi Arabia and the UAE) significantly pivot to the Yuan, the effects would be structural rather than an overnight collapse. Here is how it would likely impact the US economy:

1. Effect on the US Dollar

The primary effect would be a reduction in global demand for the dollar.

De-dollarization: Currently, central banks must hold vast USD reserves to pay for energy. If they can buy oil with Yuan, their need for dollars drops.

Currency Value: Lower demand typically leads to a weaker dollar relative to other major currencies. This would make imports more expensive for Americans (potentially fueling inflation) but could make US exports more competitive abroad.

Safe-Haven Status: While the dollar’s “reserve” status wouldn’t vanish immediately due to the depth of US financial markets, its “hegemony” would erode, making the global economy more multipolar.

2. Effect on US Interest Rates

The Petrodollar system creates a “recycling” loop: oil producers earn dollars and “park” them in liquid US assets.

Reduced “Recycling”: If Gulf nations earn Yuan instead, they will likely reinvest that capital into Chinese bonds or other non-USD assets.

Upward Pressure: A decrease in the automated buying of US assets means the US must offer higher interest rates to attract other investors to buy its debt. This could lead to higher borrowing costs for US mortgages, credit cards, and business loans.

3. Ability of the US Government to Borrow

The US government relies on the “exorbitant privilege” of the dollar to fund its large budget deficits.

Lower Demand for Treasuries: Gulf sovereign wealth funds have historically been major buyers of US Treasury bonds. If they stop “recycling” oil profits into Treasuries, the US loses a reliable, massive lender.

Fiscal Constraints: The government could still borrow money, but it would be more expensive. Higher interest payments on the national debt would consume a larger portion of the federal budget, potentially leading to tougher choices between raising taxes, cutting spending, or printing more money (which risks further inflation).

Current Context (2026)

As of early 2026, we are seeing a “multi-currency” oil market emerge rather than a total replacement.

Bilateral Deals: Saudi Arabia and the UAE have begun accepting Yuan for some shipments to China (their largest customer), but they still price the majority of their global exports in dollars to maintain the stability of their own currency pegs.

The Liquidity Gap: The Yuan still faces hurdles because it is not as “freely tradable” as the dollar. Most global investors still prefer the legal transparency and liquidity of the US financial system.

Would you like me to compare the current size of the Petroyuan market versus the Petrodollar market to see how far this shift has actually gone?

yes

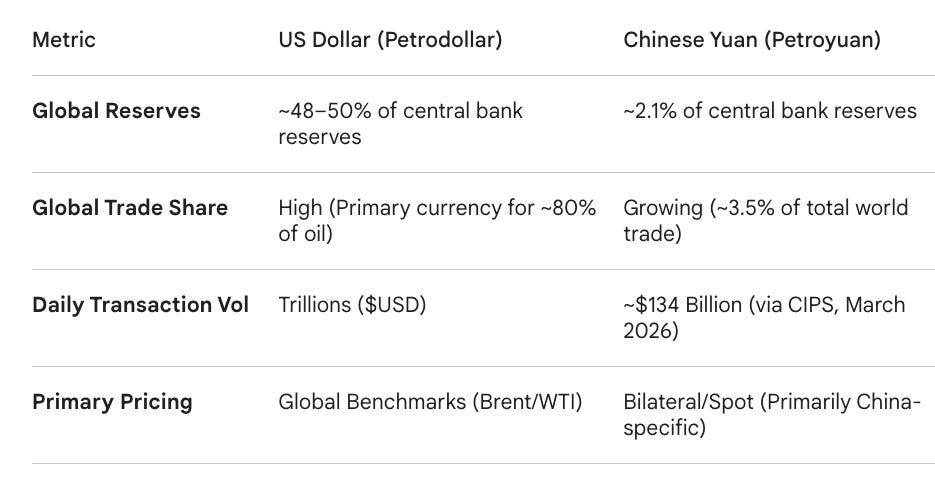

In 2026, the global energy landscape is currently at a volatile “inflection point.” While the Petrodollar remains the dominant global standard, the Petroyuan is rapidly transitioning from a theoretical threat to a functional alternative, accelerated by the 2026 conflict in the Persian Gulf.

Here is a breakdown of how the two markets currently compare in terms of scale and influence:

1. Market Share and Scale

While the Yuan is growing, the Dollar still holds a massive lead in terms of total global reserves and transaction volume.

2. The 2026 Shift: Why the “Gap” is Closing

Several factors in the first half of 2026 have significantly narrowed the gap between these two systems:

The Iran-USA/Israel Conflict: The war that began in February 2026 has made the Strait of Hormuz a “toll booth.” Reports indicate that Iran has allowed smoother passage for tankers whose trade is settled in Yuan, incentivizing buyers to bypass the dollar to ensure supply security.

Saudi Arabia’s Pivot: For the first time in 50 years, the formal US-Saudi agreement to trade exclusively in dollars has effectively lapsed. In March 2026, Saudi Aramco shipped a multi-year high of 58 million barrels to China, with an increasing portion of those specific transactions settled in Yuan to fund Saudi Arabia’s own massive infrastructure projects with Chinese firms.

Petro-Equities: A major shift occurred in 2025–2026 where Gulf nations stopped “recycling” dollars into US Treasuries (fixed income). Instead, they are moving toward “Petro-equities,” investing in global tech stocks (like NVIDIA or Apple) or Chinese equities. This breaks the traditional loop that kept US interest rates artificially low for decades.

3. The “Fragility” Factor

Despite the rise of the Yuan, the Petrodollar is currently benefiting from a “Safe Haven” effect. Because of the 2026 war, global investors are fleeing to the USD as a temporary refuge, pushing the Dollar Index to its highest level since the early 2020s.

The Paradox: The dollar is getting stronger in the short term due to war uncertainty, but its long-term foundation is eroding as countries build “sanction-proof” payment rails like China’s CIPS (Cross-Border Interbank Payment System).

Summary of the Effect

The result is a fragmented market. We are moving away from a world where one currency rules oil, toward a “bipolar” system:

The Dollar Zone: Used for global benchmarks and Western-aligned trade.

The Yuan Zone: Used for direct trade between the “Global South” (BRICS+ nations), specifically for those looking to avoid US financial oversight or sanctions.

Would you like me to look into how this shift is impacting the specific “BRICS+” expansion countries, such as the UAE or Egypt, in their 2026 trade deals?

yes

The expansion of the BRICS+ alliance in 2024 and 2025 has turned the “Petroyuan” from a hypothetical threat into a functional tool for regional trade. In 2026, countries like the UAE and Egypt are leading the charge in creating “non-dollar corridors.”

Here is how these specific countries are using the Yuan and other mechanisms to bypass the US Dollar:

1. The UAE: Moving from “Petrodollars” to “mBridge”

The UAE is no longer just “talking” about de-dollarization; they are building the digital pipes to make it happen.

Project mBridge: This is a multi-CBDC (Central Bank Digital Currency) platform connecting China, the UAE, Hong Kong, and Thailand. In 2026, it is being used to settle hundreds of millions of dollars in trade instantly, bypassing the Western SWIFT system entirely.

Non-Oil Trade Growth: Bilateral non-oil trade between the UAE and China surged to nearly $50 billion in the first half of 2025 alone. To settle this without losing money on dollar exchange fees, the UAE has increasingly used the Yuan for high-tech and infrastructure payments.

Energy Experiments: While the UAE still prices most of its oil in USD to protect its currency peg, it successfully executed its first Yuan-settled LNG (Liquefied Natural Gas) trade with China, signaling that the “petrodollar-only” rule is officially over.

2. Egypt: A Strategic Pivot for Survival

For Egypt, the shift to the Yuan is a matter of economic survival due to a persistent dollar shortage and the fallout from regional conflicts.

The Currency Swap Expansion: In March 2026, Egypt moved to double the value of its existing currency swap agreement with China. This allows Egypt to pay for Chinese imports (its largest source of goods) in Yuan, preserving its scarce US dollar reserves to pay off international debts.

Panda Bonds: Egypt became the first Middle Eastern country to issue “Panda Bonds”—sovereign bonds denominated in Yuan. This allows Cairo to tap into Chinese capital markets directly, reducing its reliance on Wall Street and the IMF.

Shielding from Conflict: As the 2026 Iran-Israel conflict disrupts traditional trade, Egypt is using Yuan-based financing to secure “green” infrastructure and manufacturing investments from China, specifically within the Suez Canal Economic Zone.

3. The “ElectroYuan” vs. The “Petrodollar”

A fascinating trend emerging in 2026 is what analysts call the “ElectroYuan.” * The Logic: While the US dominates the oil world (Petrodollar), China dominates the electrification world (solar, EVs, batteries).

The Strategy: As the UAE and Egypt transition to green energy, they are buying Chinese technology. China often bundles this hardware with Yuan-denominated financing.

Result: By 2026, these countries aren’t just switching currencies for oil; they are switching because their future energy infrastructure is built on a Chinese supply chain that prefers the Yuan.

Summary Table: 2026 BRICS+ Trade Shifts

CountryMajor Action in 2026Impact on US DollarUAEScaled up mBridge digital paymentsReduces reliance on SWIFT and USD for regional settlements.EgyptDoubled Yuan Swap line with ChinaBypasses the need for USD for its largest import partner.Saudi ArabiaLapsed 50-year “USD-only” oil pactSymbolic and structural blow; allows for “multi-currency” oil pricing.

Export to Sheets

Would you like to see how these shifts are affecting the US Treasury’s specific auction data—essentially, who is stepping in to buy US debt now that these nations are buying less?

As of early 2026, the shift you’re describing is actively playing out. With US gross debt recently eclipsing $39 trillion, the question of who buys this debt—and at what price—is more critical than ever.

When BRICS+ nations (like Saudi Arabia, the UAE, and China) reduce their “recycling” of oil profits into US Treasuries, a new set of buyers has had to step in. Here is the breakdown of who is currently picking up the slack and the cost to the US taxpayer.

1. The Shift: From “Official” to “Private” Buyers

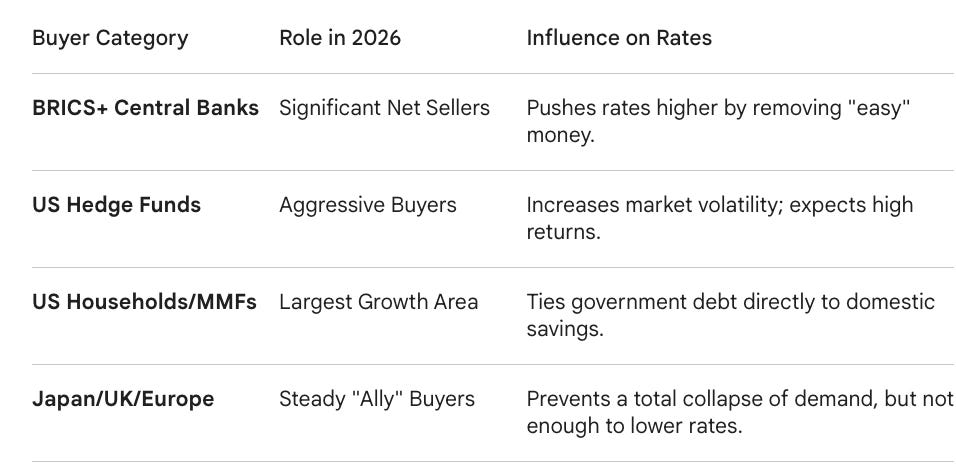

Historically, foreign central banks (the “official sector”) were the backbone of Treasury auctions. That has changed.

The Exit: Central bank holdings of Treasuries have hit a decade-level low relative to the total debt. China’s holdings, for instance, have been cut nearly in half from their peak, sitting around $680 billion as they pivot toward gold and local currency trade.

The New Guard: The primary buyers in 2025 and 2026 have shifted to private investors and domestic institutions:

Hedge Funds & Asset Managers: High-frequency traders and “basis trade” speculators now account for a massive share of auction volume.

Money Market Funds: Since 2023, these have seen explosive growth as they offer high yields to everyday investors, essentially using your savings to fund government spending.

“Allied” Nations: While BRICS sells, nations like Japan, the UK, and Canada have actually increased their holdings, acting as a regional buffer for the dollar.

2. The Price Tag: The “Term Premium”

The US government can still borrow money, but it is no longer “cheap.” Because the new buyers are price-sensitive (unlike central banks who bought for political stability), they demand a higher reward for the risk.

Higher Yields: To attract these private buyers, the Treasury has had to keep yields on 10-year notes elevated, often staying above 4% throughout 2025 and 2026.

Interest Expense: The US now spends more on interest payments than it does on its entire defense budget. This creates a “fiscal treadmill” where the government must borrow just to pay the interest on what it already borrowed.

3. Impact on US Interest Rates

The reduced demand from oil producers exerts constant upward pressure on interest rates.

If the UAE or Saudi Arabia aren’t “forced” to buy Treasuries to park their oil wealth, the US must compete with the rest of the world for capital.

This keeps mortgage rates and business loan costs higher for longer, even if the Federal Reserve tries to cut its own “policy” rates.

Summary: The 2026 Ownership Profile

The “Silent” Risk: Liquidity Volatility

The biggest concern in 2026 isn’t that the US will run out of buyers, but that the market has become fragile. Private buyers are fickle; if a geopolitical shock occurs, they sell much faster than a central bank would. This leads to sudden “spikes” in interest rates that can rattle the entire global economy in a matter of hours.

Would you like me to look into how the US Treasury is changing its “auction mix”—for example, whether they are moving toward shorter-term “Bills” to keep the market moving?

As of April 2026, the US Treasury is navigating a “high-wire act” in its borrowing strategy. To compensate for the waning demand from traditional Petrodollar recyclers (like the Gulf nations), the Treasury has fundamentally shifted how it issues debt to keep the government funded.

Here is the current breakdown of the Treasury’s 2026 “Auction Mix” and why it matters to you.

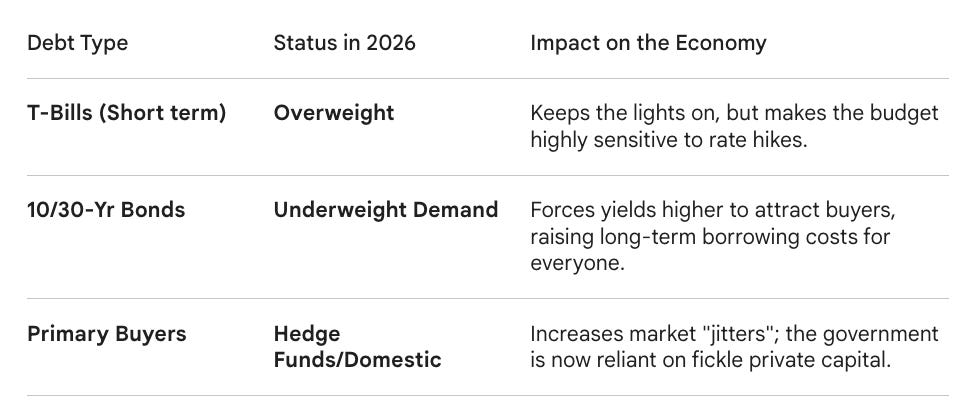

1. The Shift to “Short” Debt (The T-Bill Binge)

Because foreign central banks are no longer “automated” buyers of long-term US bonds, the Treasury has pivoted toward short-term Treasury Bills (T-Bills)—debt that matures in 12 months or less.

The Strategy: T-Bills are the most liquid assets in the world and are eagerly gobbled up by domestic Money Market Funds and private investors.

The Data: In early 2026, T-Bills make up roughly 23–25% of the total outstanding US marketable debt, well above the historical “peace-time” average of 15–20%.

The Result: This has allowed the US to continue borrowing hundreds of billions per month without causing a “failed auction” at the long end of the curve (10-year and 30-year bonds).

2. Who is Buying Now? (The Domestic Pivot)

With Persian Gulf producers and China paring back their holdings, the “face” of the US creditor has changed:

Hedge Funds & the “Basis Trade”: Large private funds have become the marginal buyers. They are not buying for “safety” like a central bank; they are buying for profit. This makes the market more volatile because these funds will sell at the first sign of trouble.

The Federal Reserve: Despite trying to reduce its balance sheet (Quantitative Tightening), the Fed has recently been forced to buy T-Bills again to ensure there is enough cash (”liquidity”) in the banking system, effectively acting as the “buyer of last resort” for the front end of the debt.

Retails & Money Markets: Everyday Americans are now a major source of government funding. High interest rates have driven trillions of dollars into Money Market Funds, which in turn buy the Treasury’s short-term bills.

3. The “Roll-Over” Risk: A Fiscal Time Bomb

While the shift to T-Bills has kept the government running, it has created a structural vulnerability:

The Refinancing Trap: Because the debt is so short-term, the US must “roll over” (re-borrow) trillions of dollars every few months.

Sensitivity to Rates: If the Fed raises rates or if there is a spike in inflation due to the 2026 Middle East conflict, the interest cost on that debt jumps immediately.

The Crowding Out Effect: The US is now spending over $1.1 trillion per year just on interest payments. This is “unproductive” spending that competes with the private sector for capital, keeping your mortgage and car loan rates higher than they otherwise would be.

Summary of the 2026 Debt Profile

Bottom Line: The US is effectively “financing a mortgage with a credit card.” It works as long as the credit card limit (investor confidence) keeps rising, but it leaves the economy extremely vulnerable to any sudden loss of trust in the dollar.

Would you like me to analyze how this “short-term debt” strategy might force the Federal Reserve to change its inflation targets later this year?

As of April 2026, the Federal Reserve is facing a “Catch-22” that hasn’t been this intense in decades. The convergence of high government debt, the shift to short-term T-bills, and the rise of the “Petroyuan” is forcing a quiet but radical debate within the Fed: Should they abandon the 2% inflation target?

Here is how the Fed’s strategy is likely to shift later this year:

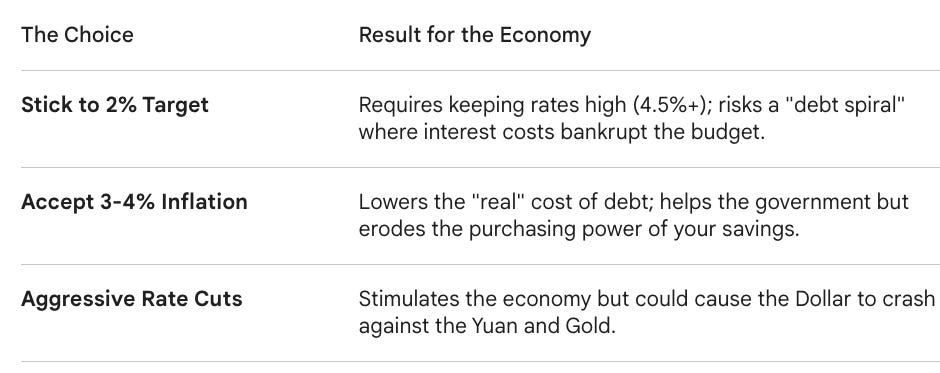

1. The “Soft” Target: Moving to 3%?

While the Fed officially maintains a 2% target, the reality of 2026—marked by Middle East conflict and high interest on debt—makes that goal nearly impossible to hit without causing a massive recession.

The Forecast Gap: In March 2026, the Fed projected inflation would hit 2.7%, but the OECD recently countered with a “jaw-dropping” 4.2% forecast.

“Opportunistic Disinflation”: Analysts believe the Fed may move toward a policy where they “accept” 3% inflation for several years. By allowing prices to rise slightly faster, the government effectively “inflates away” the real value of its $39 trillion debt, making those massive interest payments easier to manage.

2. The Fed as the “Hidden” Buyer

Because Persian Gulf nations are recycling fewer dollars into Treasuries, the Fed is being pulled back into the bond market.

Ending the “Runoff”: In early 2026, the Fed discontinued the “runoff” of its balance sheet (Quantitative Tightening).

Reserve Management: To keep the T-bill market from freezing up, the Fed has started “reserve management purchases”—buying up to $40 billion per month in short-term debt. This isn’t called “Quantitative Easing,” but the effect is the same: the Fed is printing money to ensure the Treasury can keep borrowing.

3. The May 2026 Leadership Cliff

A major “wild card” is the expiration of Jerome Powell’s term as Chair on May 15, 2026.

The Transition: Markets are bracing for a new Chair who may be more “dovish” (favoring lower rates even if inflation stays high) or more politically aligned with the need to fund the deficit.

The Market Reaction: Any signal that a new Chair will prioritize “debt sustainability” over “price stability” could cause the dollar to weaken further, accelerating the shift toward the Yuan for global trade.

Summary of the Fed’s 2026 Dilemma

The Treasury is currently walking a tightrope. If the “Petroyuan” continues to gain ground, the US loses its ability to export its inflation to the rest of the world.